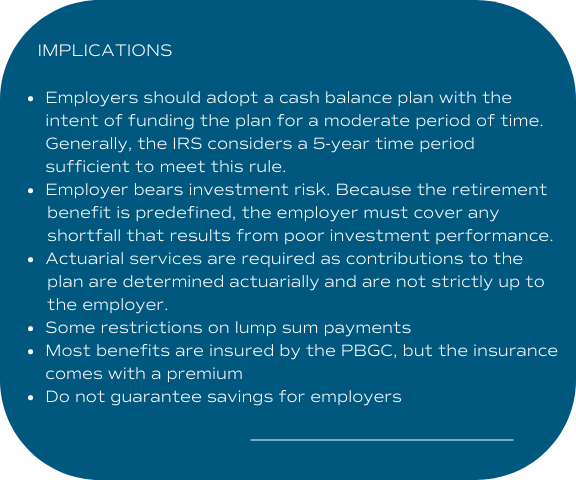

A cash balance plan is a hybrid between a defined contribution plan, such as a 401(k), and a traditional defined benefit plan. Cash balance plans provide a promised benefit in the form of an account balance.

How Do Cash Balance Plans Work?

Each Year, a participant’s account is credited with a “pay credit” and an “interest credit”. A pay credit can be a percentage of compensation, set dollar amount, or a combination of both. An interest credit is either a fixed rate or variable rate that is linked to an index. That cash balance plan document will define group pf participants and their “pay credit”. At retirement, cash balance plan participants have the option to receive their account balance as an annuity for life or as a lump sum.

5 questions to consider

Does the employer already maximize their contributions to a defined contribution plan?

Do the highly compensated employees (HCEs) wish to contribute far more than the defined contribution limits will allow?

Is there a low ration of non-highly compensated employees to highly compensated employees?

Are the highly compensated employees older than the non-highly compensated employees, on average?

Will the employer have significant and consistent cash flow moving forward?

If you’ve answered yes to most of these questions, a cash balance plan could be the right fit. Please contact us so we can discuss your specific situation. We look forward to hearing from you!